Metropolitan Transport Information System

by Digital Geographic Research Corporation

25+ years innovating

- HOME

- PRODUCTS & SERVICES

- RESOURCES

News & Commentary News & Press Reports Light Technical Geography 80-20 (nuggets for adults) Geography Kids' Hangout Technical METRIS Publications GIS Publications Associated projects NCRST VITAL

- ABOUT

Turn Time — Slow Gains

From the standpoint of truck turn time, recovery from the 2014 port meltdown in southern California is certainly under way, but it's slow.

Background

TURN TIME RESOURCES

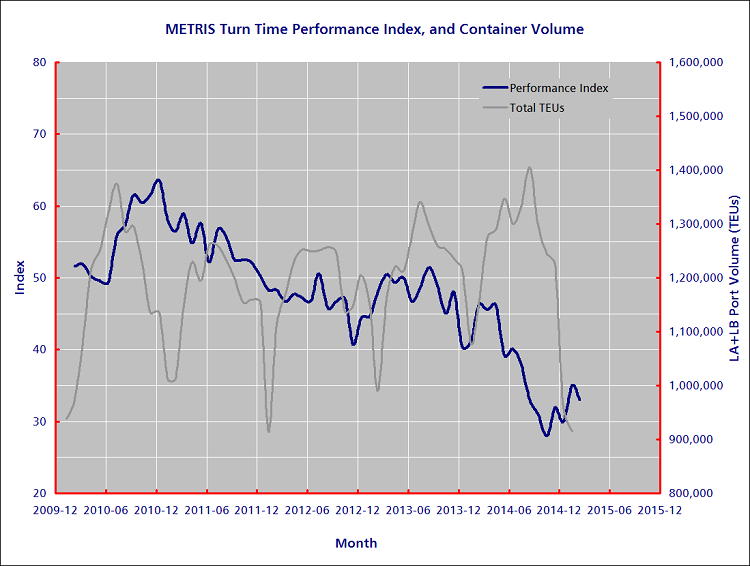

For the past three months, I've refrained from issuing turn time updates. There's no question that turn time has been miserable, breaking below 30 on the 100-point scale of the METRIS Turn Time Performance Index, with nearly 40% of truck visits taking over 2 hours in November. As a point of reference, back in 2011, 15% of visits were over 2 hours. I called that the Exception Rate. Two hours ceased to be a threshold of exceptionalism more than a year ago.

But to place this in context, we're talking in hours. Turn time was eclipsed as an issue by (a) backlogs that delayed containers by days and even weeks, throwing off scheduling of not just goods deliveries but also empty-container returns and chassis, even trains — the entire freight system, and (b) a catastrophic drop in traffic, that will penalize not just truckers but the entire port community well into the future.

The troubles were attributable to several factors, in particular recovering post-recession trade volume, mega-vessels, chassis and severe labor problems. Much of this had been brewing over a period of time. Trade volume was swelling gradually; the ports' operational elasticity was effectively decreasing: vessel size had grown over decades, deluging terminals with bursts of volume that triggered more and more frequent episodes of overwhelming congestion; and the chassis timebomb had been counting down for two years.

Only the labor problem was new to 2014. Surfacing just after turn time performance had already hit a low in September, its timing was devastating. In November the METRIS Index bottomed out at 28 (Figure 1).

Recent Data

So after the PMA-ILWU agreement was struck on February 20, it was heartening to see an immediate and substantial improvement in turn time. February saw the best month-to-month gain in the past year.

That may have created some inflated expectations. I for one was eagerly anticipating even better March numbers. They might indicate a strong bounce back to productivity. And on the lighter side, they'd have been the definitive counterpoint to the ILWU's contention that they'd never slowed anything down.

But turn time worsened slightly in March. Within the margin of statistical uncertainty it was on par with February. So what do we conclude?

- Either the ILWU had a point and labor's role in the slowdown was exaggerated, or it persists, or it's overshadowed by a cargo backlog and/or ongoing operational difficulties. At any rate, conclusion of the longshore contract negotiation was not a Mary Poppins snap of the fingers that restored everything to a neat and tidy state.

- The chassis pool of pools and the empty-container yard are laudable initiatives, but it's early for their effects to be felt.

- There was a huge rise in the number of truck visits recorded by METRIS in March, compared with February. Conceivably there were gains in efficiency after all, that were trumped by volume-generated congestion. The choke point shifted from the outer harbor (queued vessels) to the terminal aisles (queued trucks). While its passage through the system is painful, it may presage relief.

- Over the past couple of years, the relationships among turn time, container volume and labor expenditures have been remarkably well defined. The delicate equilibriums — in practical terms, stability, predictability, the degree to which we can look at A and draw conclusions about B — were shaken by the events of late 2014. Compounding that, there's been a freight flight out of southern California and the west coast, that coincided with the Chinese New Year. Combined volume at the ports collapsed from 1.4m TEUs in September 2014, nearly the busiest September ever, to 0.96m TEUs in January 2015, the lowest January since 2002. This is massive upheaval in a very short time, hence a hazardous time for analysis, let alone punditry.

Conclusion

There's still a lot of turbidity in the numbers. Due to the convergence of numerous positive and negative forces, it's impossible to trace cause and effect. It will take a little more time for the regular dynamic rhythm to be re-established, and trends to become clear. Turn time is still abysmal, scoring 33 on the METRIS Performance Index in March. Recovery of the ports' health remains the bigger issue. I don't doubt for a moment that it will bounce back. The question is how quickly, and whether that pace, fast or slow, will have other ramifications.

Tweet this page Follow @METRISnews

Citations

“LA, Long Beach drayage turn times 'substantially' improving, analysis shows.” Journal of Commerce, 2015 04 14

Acknowledgments

The METRIS data archive, on which this article is based, was possible due to the cooperation and patronage of leading drayage carriers who have been our partners over the past 8 years: Ability/Tri-Modal, California Intermodal Associates, Dependable Highway Express, Fox Transportation, G&D Transportation, Golden State Express, Harbor Division Inc, LA Grain, Port Logistics Group, Price Transfer, Progressive Transportation Services, Southern Counties Express, TK Transport, TTSI and Yamko Truck Lines.

Comments

Add Your Comment

Related

TURN TIME RESOURCES