Metropolitan Transport Information System

by Digital Geographic Research Corporation

25+ years innovating

- HOME

- PRODUCTS & SERVICES

- RESOURCES

News & Commentary News & Press Reports Light Technical Geography 80-20 (nuggets for adults) Geography Kids' Hangout Technical METRIS Publications GIS Publications Associated projects NCRST VITAL

- ABOUT

Turn Time — in the Doldrums?

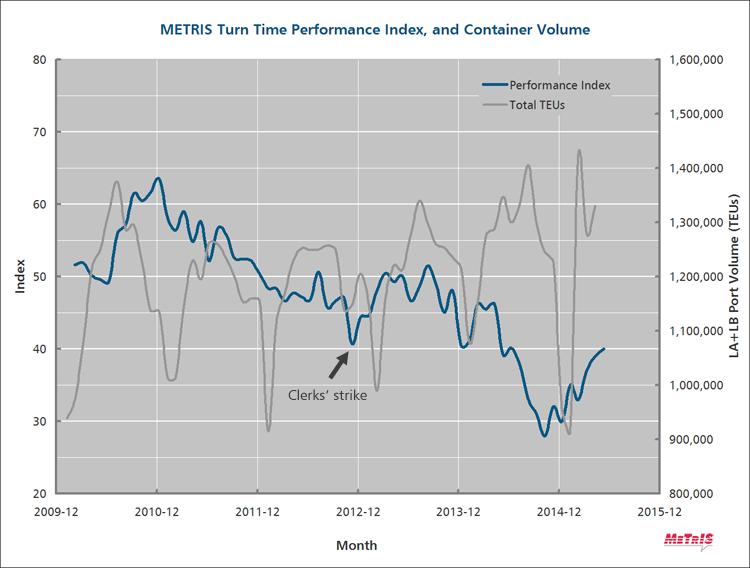

Turn time at LA/LB is on the mend. It has certainly bounced back from November 2014 when it bottomed out at 28 on the METRIS 0-100 Index. In June 2015 it stood at an 11-month high of 40.

TURN TIME RESOURCES

Do the gains mean that the chassis problem has been solved? That vessel size was never a factor? That labor relations are back to normal? That new delivery methods are having an impact? It's impossible to draw any of these conclusions looking at turn time alone. A better justified conclusion is that at least some of 2014's problems are lingering.

A METRIS Index of 40 is a D– at best; some would argue an F. It's on par with December 2012 (the backlog and chaotic aftermath of the clerks' strike) and June 2014 (the worst month on record at the time). Prevalence of 6-hour visits remains troublesome, around 1%. There's a long way to go.

A glance at the tail end of the graph (Figure 1) seems to indicate that the recovery is running out of steam, and leveling off. There's talk about this being the “new normal,” the doldrums. Is this valid?

There are reasons to be more optimistic:

- This is no longer a systemic malaise. The residual problems are largely confined to three terminals. At the other terminals, performance isn't back to what it was a couple of years ago, but it's trending positively.

- Volume is near record levels, and has been oscillating wildly from near-record high to near-record low and back again. On the surface, uncertainty is not conducive to gains in performance. But the volume drops in January and February were a boon that helped the system clear the backlog. A sustained upward macro-trend in productivity, at a time of record traffic, even if slow, is good news.

- There are worse problems to have than record volume.

The geographic fundamentals of LA/LB — location, infrastructure, skilled labor supply, rail connectivity — are overwhelmingly strong. What got tested in 2014 was its operating capacity, that was temporarily diminished by unusual events. It's not the same as a loss of physical capacity, which would be a longer-term problem, and a reason to look elsewhere. The challenge for industry leaders is to keep the recent operational difficulties from looking like they'll become permanent.

Tweet this page Follow @METRISnews

Citations

“LA-LB terminals graded D-minus despite better truck turn times.”

Journal of Commerce, 2015 07 07

[DGRC clarification: the D– is not assigned to terminals alone, it's the efficiency of port performance as a whole,

and reflects on all those whose actions impact it, from policy makers to BCOs to longshoremen.]

Acknowledgments

The METRIS data archive, on which this article is based, was possible due to the cooperation and patronage of leading drayage carriers who have been our partners over the past 8 years: Ability/Tri-Modal, California Intermodal Associates, Dependable Highway Express, Fox Transportation, G&D Transportation, Golden State Express, Harbor Division Inc, LA Grain, Port Logistics Group, Price Transfer, Progressive Transportation Services, Southern Counties Express, TK Transport, TTSI and Yamko Truck Lines.

Comments

Add Your Comment

Related

TURN TIME RESOURCES